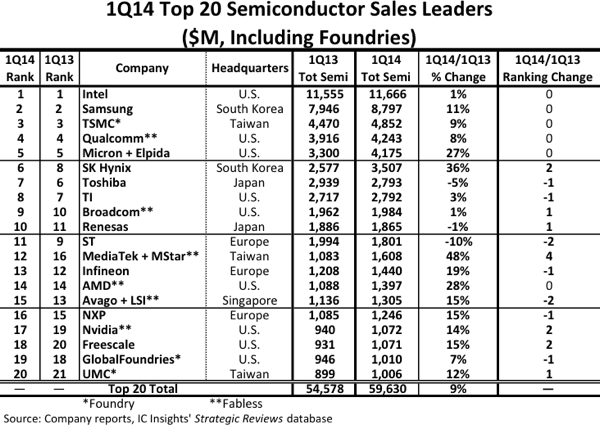

In Figure 1. The top 20 worldwide semiconductor sales ranking for 1Q14 includes nine suppliers headquartered in the U.S., three in Taiwan, three in Europe, two in South Korea, two in Japan, and one in Singapore, a relatively broad representation of geographic regions.

The top-20 ranking includes three foundries (TSMC, GlobalFoundries, and UMC) and six fabless companies. It is interesting to note that the top four semiconductor suppliers all have different business models. Intel is essentially a pure-play IDM, Samsung a vertically integrated IC supplier, TSMC a pure-play foundry, and Qualcomm a fabless company.

Foundries and fabless companies are clearly identified in Figure 1.

After Avago’s purchase of LSI Corp. on May 6, 2014, the combined annual semiconductor sales run-rate of the two companies is likely to be over $5 billion.

Also, last year’s Micron/Elpida merger essentially created a new “giant” semiconductor company with Micron’s sales expected to be over $17 billion this year!

In total, the top 20 semiconductor companies’ sales increased by 9% in 1Q14 as compared to 1Q13.

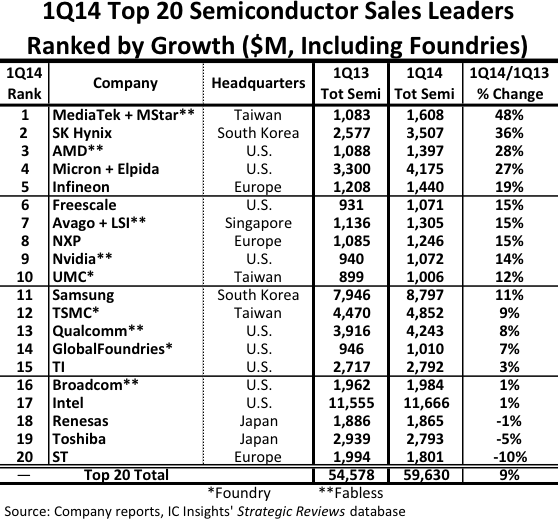

Figure 2 shows year-over-year growth rates among the 1Q14 worldwide top 20 semiconductor suppliers .

The success of the fabless business models and the continued strong growth of the memory market are evident .

As shown, 10 of the top 11 1Q14 performers were either memory suppliers (SK Hynix, Micron, and Samsung) or fabless companies (MediaTek, AMD, Infineon, Freescale, Avago/LSI, NXP, and Nvidia).